You may have heard that property values are on the decline. But what does this mean if you’re planning to refinance? We’ll discuss how falling housing prices may affect your refinancing application and what you can do about it.

With the rising cost of living and climbing interest rates, you may be looking to refinance your mortgage.

Depending on your circumstances, it can be a great way to get a better interest rate on your loan.

Not to mention that if you need access to funds for an investment property or renovation, refinancing can allow you to cash out equity in your home to use for other purposes.

But, according to CoreLogic, 79.5% of house and unit market values are on the decline across Australia. And this can affect refinancing outcomes.

We’ll walk you through just what the effects of a property value drop can mean for refinancers and how you can take action now to get ahead of the curve.

Refinancing and your property’s value

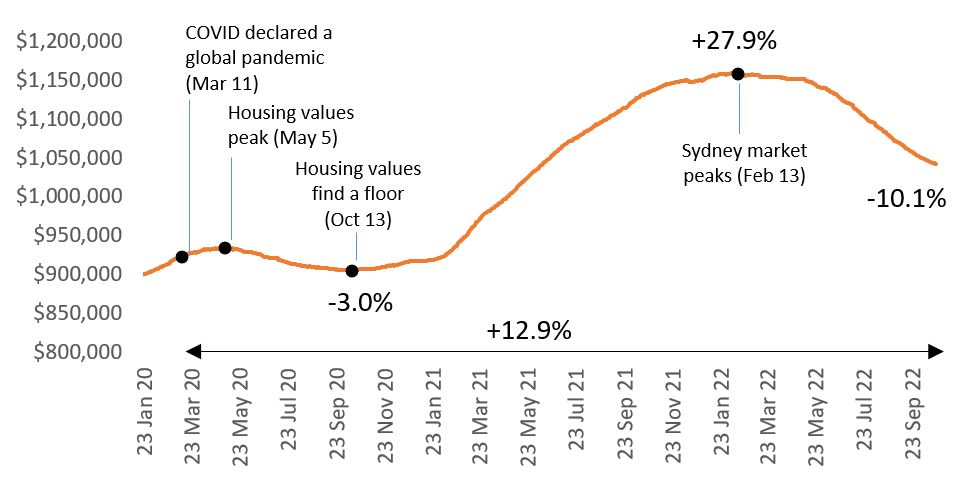

Rising rates have contributed to declining property values in some areas around the country.

For example, Sydney property prices have declined 10% since they peaked in February this year, according to the latest CoreLogic data, and many economists believe they’ll fall even further.

And as a homeowner, a drop in property value can affect your equity.

That’s because equity is the difference between your property’s (market) value and your mortgage balance. And it’s a number that lenders pay attention to when assessing refinancing applications.

Refinancing before your equity drops may see your refinancing application have a greater chance of success.

You see, most lenders will typically require you to have 20% equity in your home to refinance, which essentially serves as a deposit.

And according to this graph here, if you’ve bought a house in Sydney (for example) since June 2021, due to the recent property price declines you soon may no longer have 20% equity in your home.

{kind=link}

If you don’t have 20% equity, you could still refinance by paying lenders mortgage insurance – but that would likely defeat the purpose of refinancing in the first place.

And if you fall into negative equity – where your home’s value drops below your mortgage balance – then refinancing most likely won’t be on the cards at all and you’ll be stuck with your current lender.

So, if you’re interested in refinancing your loan to get a better rate, sooner may be better than later … depending on how your property value is fairing.

Refinancing to cash-out equity

If you’re keen to unlock some equity – you’re not alone!

According to NAB research, seven in 10 mortgage holders recently cashed out equity while property prices were high and used the money to renovate, invest in property or shares, or boost their superannuation

So how does cashing out equity work?

Let’s say you bought an $800,000 house five years ago that is now worth $1 million.

And let’s also say you took out a $600,000 loan for that house, which you’ve managed to pay down to $500,000 (you little beauty!).

By refinancing that $500,000 loan into an $800,000 loan (banks will typically let you borrow up to 80% of a property’s market value), you can unlock $300,000 in equity.

However, if you delay a year or so, and national property prices decline 10% over this period, your house might only be valued at $900,000.

That would mean if you wanted to unlock 80% of your property’s market value, you could only refinance your $500,000 mortgage into a $720,000 loan – and therefore only unlock $220,000 in equity.

Get in touch

If you’ve been considering refinancing lately, contact us to find out more. Whether you’re looking to land a better rate or unlock equity in your home, we can help you with all the particulars.

Disclaimer: The content of this article is general in nature and is presented for informative purposes. It is not intended to constitute tax or financial advice, whether general or personal nor is it intended to imply any recommendation or opinion about a financial product. It does not take into consideration your personal situation and may not be relevant to circumstances. Before taking any action, consider your own particular circumstances and seek professional advice. This content is protected by copyright laws and various other intellectual property laws. It is not to be modified, reproduced or republished without prior written consent.

Share

Previous Article

Is now a good time to buy an investment property?

Next Article

Hold your horses: RBA hikes cash rate again to 2.85%